By CPA Alfred Okwee

Ag. Chief, Finance and Grants Management,

The AIDS Support Organization (TASO)

The pass rates for Financial Accounting - Paper 1 over the recent sittings have, in some cases, been average (December 2022 - 48.68% while June 2022 - 56.95%). This article provides some tips to improve your chances of passing this paper. These tips come in two sections; (1) what to know prior to the examination and (2) during exams.

(1) Prior to the examination:

- Understand and appreciate the entire syllabus. Focus on comprehensively covering the syllabus as you revise/prepare for the exam.

- Practise as many questions on the different areas of the syllabus as possible to improve your time and accuracy.

- Read relevant materials shared by the Institute for this paper, for example, the examiner’s comments posted on the website and attend the student engagement seminars on Financial Accounting. These materials and platforms provide valuable information to help a candidate to pass.

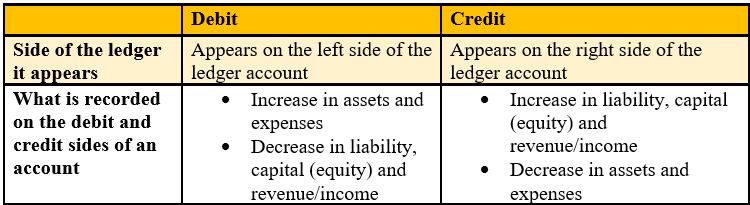

- Appreciate and understand ALL aspects of the double entry principles because it is the basis for all computational questions and some of the theory questions. Recall the double entry rules below:

Understanding the double entry principles will enable a candidate to:

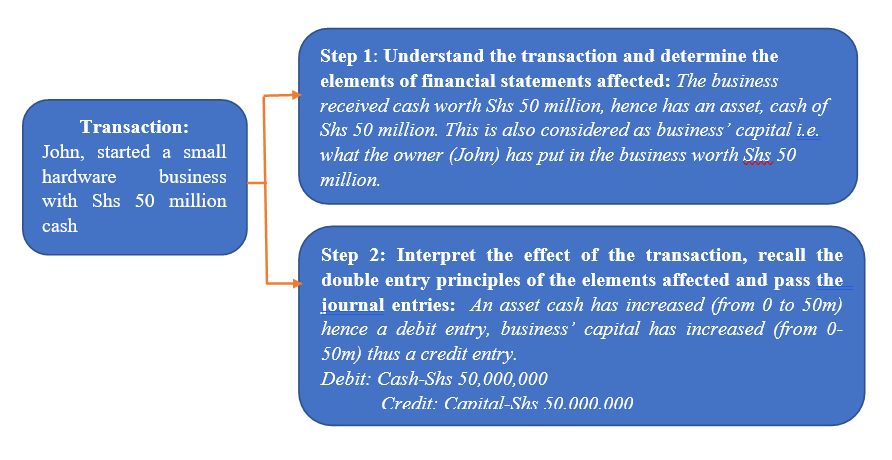

(i) Make correct entries in the ledgers, balance the accounts and extract a trial balance without errors.

Illustration: Consider this transaction: John started a small hardware business with Shs 50,000,000 cash. You can follow the suggested steps below to understand the process to pass the correct double entry.

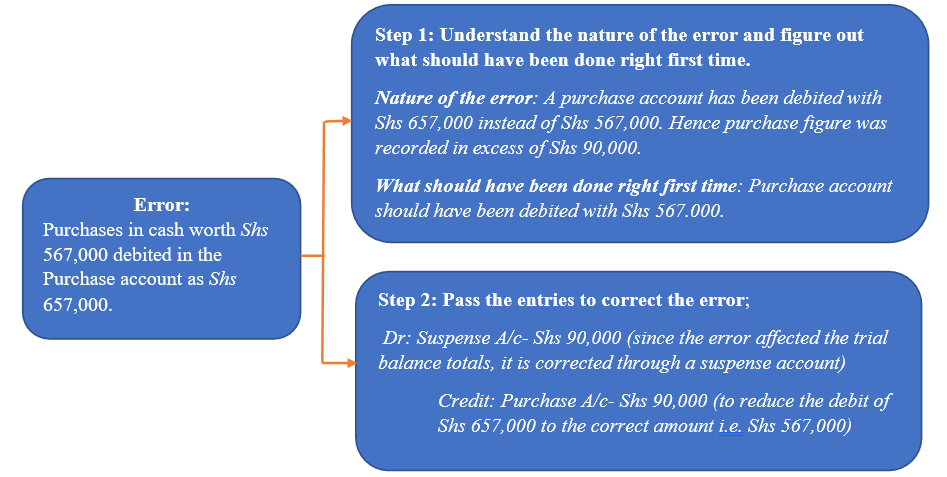

(ii) Deal with errors correctly when faced with some of the errors i.e. pass the right journal entries to correct errors and incorporate additional information to the accounts.

Illustration. Consider the following error. Purchases in cash worth Shs 567,000 was correctly credited to the cash book but debited in the Purchase account as Shs 657,000;

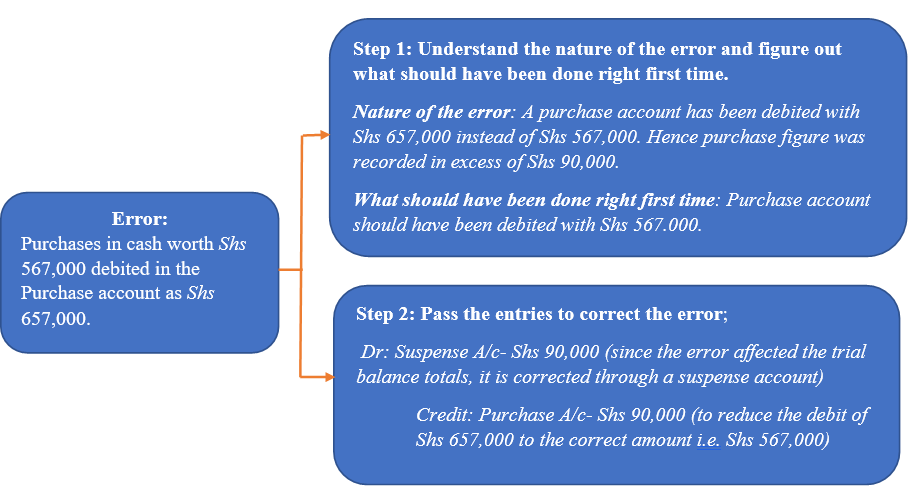

(ii) Deal with errors correctly when faced with some of the errors i.e. pass the right journal entries to correct errors and incorporate additional information to the accounts.

Illustration. Consider the following error. Purchases in cash worth Shs 567,000 was correctly credited to the cash book but debited in the Purchase account as Shs 657,000;

(2) During the exam:

- Plan your approach well (order of questions to attempt during the exam) during the first 15 minutes of the exam (allocated for ONLY reading through the paper). Read through the question paper to choose which questions to attempt. It is advisable to start with questions you are knowledgeable and comfortable with, for example, the questions where you are sure of raising the average mark or more.

- Manage your time well. Remember, there are 5 questions carrying 20 marks each to be attempted in 180 minutes (3 hours). This implies that each question should take approximately 36 minutes i.e. (180 minutes/5 questions). Please note that Section A - 20 Multiple Choice Questions (MCQs) is equivalent to 1 question of 20 marks. Section A should also be done in 36 minutes or less.

- When attempting a computational question in section B, it is advisable to read what is required of the candidate first before reading the body of the questions. This enables a candidate to then read the body of the question with a correct mindset. For instance, a question may contain a trial balance and candidates may be required to prepare a redrafted trial balance. A candidate who has not read what is required of him/her may be tempted to think he/she is required to prepare full financial statements as he/she reads the question and hence set up the layout to include financial statements. This candidate would have wasted time setting such a layout. Reading what is required of you enables you to get it the first time and hence avoid such instances that lead to time wasting and no marks.

- Try to attempt all questions required within the available time. Answer ALL MCQs and do not attempt to “investigate” why your answer did not balance if you still have questions to attempt. Rather than investigate, I recommend the candidate proceeds to attempt the next question.

- Show all your workings clearly. Marks are allocated for workings as well.

- Stay calm throughout the exam, and do not panic. You are in a better position to think clearly and remember what you have read when you are calm.

Wish you the very best as you prepare to sit for Financial Accounting