What you should know about sustainability reporting

By CPA Elizabeth Kaheru & CPA Lydia Nankabirwa

Technical Officers,

ICPAU

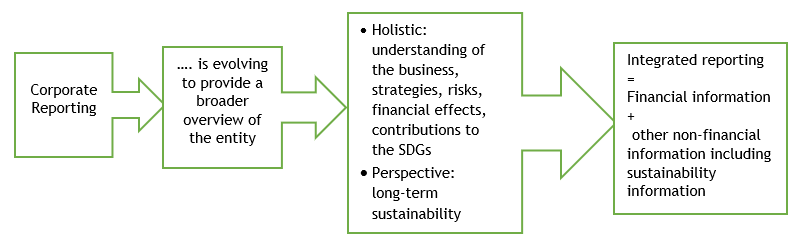

Sustainability reporting broadly refers to the disclosure and communication of an entity’s environmental, social, economic and governance impacts. The information is communicated through a document called an annual report. An annual report means a document that contains the audited financial statements and other information relevant to the understanding of the nature, objectives, performance and results of an entity during a reporting period. Financial and non-financial information is integrated within this single document.

A sustainability report is now regarded as a key element of the annual report and examines how other non-financial aspects contribute to or influence an entity’s value creation process. Sustainability reporting gives an overview of an entity’s economic, environmental and social impacts, and allows the annual report user to get a complete picture of its activities and impact.

Components that support sustainability reporting

The African Regional Partnership (ARP), a partnership established with the support of UNCTAD[1] to promote harmonisation and improvement of sustainability reporting and SDG reporting in Africa, identified three components that support the sustainability reporting infrastructure:

- Regulatory component – a supporting legal and regulatory framework, which includes the use of: International Standards (IFRS, IPSAS, ISA), Codes (Corporate Governance Code, Code of Ethics), and best practices.

- Institutional component - the existence of professional associations and/or standards setting bodies such as the Institute of Certified Public Accountants of Uganda (ICPAU), and regulatory bodies (such as Capital Markets Authority, Uganda Securities Exchange, Insurance Regulatory Authority).

- Human capacity component - building capabilities and preparedness across entities of different sizes through an educational system focused on sustainability reporting at both the professional level and continuing professional development.

Presently, sustainability reporting initiatives exist in silos and are non-existent in many sectors, with businesses more concerned with immediate profitability without recourse to socio-environmental consequences. There is also a lack of uniformity in the reporting practices among entities. This could be attributed to different sustainability-related reporting frameworks in existence currently and the lack of knowledge/ awareness of these frameworks.

The most commonly used frameworks at present are:

- The Global Reporting Initiative (GRI) standards. The GRI developed the first corporate sustainability reporting framework. These Standards have been accepted globally, and a large percentage of entities (including some in Uganda) report on their sustainability impacts using the GRI Standards. This is because they are dedicated to providing information to as many stakeholders as possible, cover a wide range of information, and provide a flexible framework for companies regardless of their size.

- Recommendations of the Taskforce on Climate-related Financial Disclosures (TCFD).

- Integrated Reporting (IR) Framework, following guidelines created by the International Integrated Reporting Committee (IIRC).

- Standards issued by the Sustainability Accounting Standards Board (SASB). These are aimed at the disclosure of material sustainability information for investors in mandatory filings and aim at identifying material sustainability factors, which are likely to impact the financial performance of an entity.

In Uganda, voluntary disclosure of sustainability information by entities has been encouraged through the annual Financial Reporting (FiRe) Awards held to reward excellence in corporate reporting. This is because there are no requirements yet by the Accounting Standards for the inclusion of disclosures in the Financial Statements.

However, with the establishment of the International Sustainability Standards Board (ISSB) under the International Financial Reporting Standards (IFRS) Foundation and ICPAU’s statutory mandate to develop or adopt standards in this regard, the Institute will collaborate with the Foundation and subsequently adopt sustainability standards issued by ISSB. Therefore, we expect uniformity in sustainability reporting practices of entities in Uganda going forward. The ISSB will deliver a global baseline of sustainability disclosures to meet capital markets needs.

The bottom line is that the sustainability report should be prepared using an established sustainability reporting framework.

Disclosure of sustainability issues in corporate reporting

Sustainability reports are presented in a variety of forms, including as corporate social responsibility (CSR) reports; health and safety reports; or environmental and community reports all integrated into the annual reports.

A preparer may disclose sustainability information and data in the annual report or in a separate sustainability report. The reporting period should be in alignment with the same financial period.

The report provides a detailed account of an entity's sustainability performance for the period, with a focus on four indicators: economic, environmental, social and governance/institutional issues. Examples of disclosures are:

- Economic indicators such as revenue, value added statement, taxes paid, green investment, community investment, research and development, and procurement practices detailing the entity’s competitive positioning and value creation process.

- The environmental indicators such as resource use efficiency - water, energy and paper, renewable energy, waste management practices, and greenhouse gas emissions management show the impact of an organisation on the environment. Reporting on climate change has become one of the most important issues in sustainability reporting.

- Social focus areas deal with how the entity manages its relationships with stakeholders such as employees, suppliers and customers. Disclosures here include training and development expenditure, employee health and safety, equity, gender and diversity issues, employee well-being and human rights, community engagement and support of social issues, and supply chain oversight.

· Governance/institutional indicators report on the internal systems and processes an organisation uses to govern itself. Disclosures include the number of board meetings and attendance, leadership diversity, number of audit committee meetings and attendance, board and executive remuneration, ethical considerations and regulatory compliance.

Why is sustainability reporting important and useful for an organisation?

It is important for organisations to have a strong focus on sustainability reporting, and with dedicated teams because it enables the organisation to measure, understand and assess its performance.

Sustainability reporting;

- strengthens an entity’s long-term strategy, thereby increasing value creation.

- improves corporate confidence and reputation, as the entity will be seen to be committed to ethical, environmental and social causes.

· demonstrates leadership, as sustainability reports can be useful tools in supporting decision-making.

Sustainability is a growing concern for organisations, regardless of whether they have a high or low impact on the environment. Therefore, organisations should adopt sustainability reports to inform stakeholders about their sustainability initiatives. This allows stakeholders to better understand the organisation's strategy and support the Board and management in the smooth implementation of these strategies.

[1] United Nations Conference on Trade and Development